A new approach to microfinance

Traditional microcredit has had limited success at enabling farmers to expand the cultivation of risky but profitable cash crops. A new approach that uses local intermediaries and aligns their incentives with farmer profits could generate better outcomes for agricultural production and incomes

Traditional microcredit has had limited success at enabling farmers to expand the cultivation of risky but profitable cash crops. A new approach that uses local intermediaries and aligns their incentives with farmer profits could generate better outcomes for agricultural production and incomes

In his Independence Day address to the nation, Prime Minister Narendra Modi unveiled an ambitious scheme of financial inclusion – the Pradhan Mantri Jan Dhan Yojna (PMJDY). The PMJDY will provide banking services to the 40% of Indians who are currently unbanked. Besides providing bank accounts and debit cards, the scheme will provide overdraft, credit and insurance facilities, and allow account-holders to receive government transfers through the bank, thus replacing money-lenders and commission agents, and reducing corruption.

Why chase financial inclusion?

While providing the poor with bank accounts could possibly bring many benefits, it is useful to take a step back and think about the ultimate goal. Although formal banks may be willing and able to open bank accounts for everyone and thus provide the technology by which the poor could conduct financial transactions, the underlying problem is that the poor have limited access to formal finance. While banks may be willing to route transfers through the new bank accounts, they are unlikely to want to start lending to all their new account-holders. As is well-known, formal banks find it difficult to identify the good borrowers. Government-led rural credit programmes have largely failed because they are unable to incentivise the borrowers to repay. The PMJDY, as currently formulated, is unlikely to solve this problem. However, as we argue below, merely providing access to finance in rural areas is also not enough. It is important also to consider who within the rural settings receives access, and on what terms. That, in turn influences how the finance is utilised, and its effect on the development indicators that we care about.

Microcredit, both as delivered by microfinance institutions (MFIs) and by bank-financed self-help group (SHG) schemes, has significantly improved the poor’s access to credit, and has done so in a financially sustainable manner. It utilises innovative ways of harnessing local relationships and social capital to identify poor but creditworthy borrowers, and incentivises them to repay their loans. Repayment schedules are rigid and instalments are due at a high frequency, often starting just a few weeks after the loan is given out. Groups are jointly liable for loan repayment, which encourages intensive monitoring by peers, and by MFI and bank officials, and discourages a borrower from investing the loan in risky projects. But agriculture is a risky business, and most agricultural projects have relatively long gestation lags. For most cash crops, revenues are realised only three or four months after planting, and so if the loans are used for agricultural working capital, borrowers must find other (costly) ways to keep up with their repayments. This can help to understand recent experimental results that microcredit does not significantly increase the incidence of entrepreneurship, or of productive activities that cause incomes to increase.

Promoting cultivation of risky cash crops

Clearly a radically different approach is needed if we are to increase rural financial inclusion in a way that enhances agricultural incomes. One approach is to modify the existing microcredit model by leveraging the information that local intermediaries have about the creditworthiness of rural borrowers. These individuals could be recruited as commission agents and asked to recommend borrowers to the lender. Their commissions would depend on the loan repayment behaviour of the borrowers they recommend. In turn this would incentivise them to identify suitable borrowers and monitor their loan repayment. If these intermediaries are traders or sellers of inputs, they could also help farmers with production and marketing, and enable them to increase their output.

To promote their use for agriculture these loans would also need to be modified in other ways. Loan disbursement and durations would need to be synchronised with crop cycles. Instead of making a group of borrowers jointly liable for the loan, borrowers would be liable individually, so that they are not held back from investing in high-risk high-return projects. Compulsory group meetings and savings requirements also discourage productive borrowers from participating in microcredit, so these would need to be removed as well.

But the proof of the pudding is in the eating. So to see how such an approach would work in practice, we designed the TRAIL (Trader-Agent Intermediated Lending) scheme, and collaborated with an MFI to implement it in a set of randomly selected villages in West Bengal. The MFI lent to individuals rather than groups. Loans were designed to be flexible and to encourage responsible behaviour: borrowers could use the loans for any purpose they wished, but the durations matched the cash crop cycles, and future credit lines were linked to past loan repayments. A local intermediary, identified from a list drawn up of traders/lenders/shopkeepers, who each had an established business and a sizeable clientele within the village, was randomly chosen to be the MFI’s agent. He recommended borrowers to the MFI, a random subset of whom then received the TRAIL loans. The interest rate on the loans was set at 18% per year, below the average informal market rate of 25%. Agents stood to earn 75% of the loan repayments as their commission. Importantly, the scheme also provided borrowers with index insurance against unexpected low crop yields or revenues1.

In another set of randomly selected villages the MFI introduced its own, traditional group-based lending (GBL) approach that involved joint liability, monthly group meetings, and savings requirements. Even the GBL loans had four-month durations, and the same 18% interest rate.

Intermediated loans vs. group-based lending

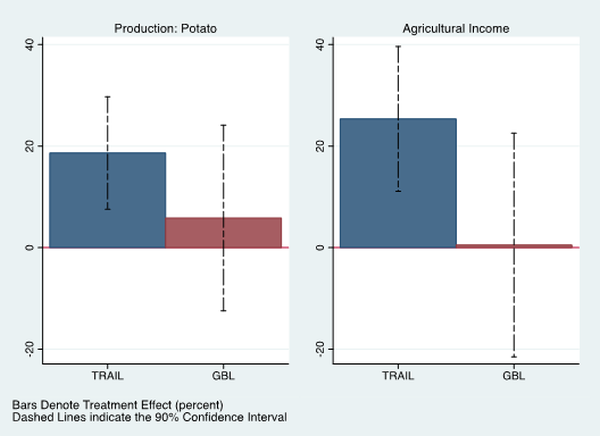

We then used detailed survey data from 2,400 households to analyse the impact of the TRAIL loans on borrowers’ cultivation, output and incomes. We find that TRAIL loans caused borrowers to expand their cultivation of potatoes and produce 17% higher output. As a result, their imputed profits from potatoes increased by 20%. Importantly, they were not substituting away from other crops; instead overall farm incomes increased by 25%. In contrast, the GBL loans had no effect on the average acreage, output and profits from agriculture.

What caused these differential impacts? Our analysis shows that not only did agents recommend individuals who had borrowed from them in the past, but within this group, they tended to recommend the more productive, and therefore safer, borrowers. TRAIL borrowers had rates of return on potato cultivation in excess of 80%, and paid lower than average interest rates in the informal credit market. In the absence of a similar screening mechanism, both low- and high-productivity borrowers participated in the GBL scheme.

Our results are also consistent with the hypothesis that agents assisted borrowers through advice about cultivation, and provided marketing services to them, since that in turn would have increased agents’ business profits. However, importantly, we do not find any evidence that the TRAIL agent exploited the borrowers. The TRAIL design limited the agent’s direct involvement in loan disbursal and recovery: his role was limited to recommending borrowers, and then receiving the commissions that varied with their repayment behaviour. Although we cannot rule out lump sum transfers from borrowers to the agent behind-the-scenes, we do not find evidence that he extracted borrower’s benefits by paying lower prices for produce he bought from them, or charging higher prices for inputs he sold to them.

Figure 1. The impact of TRAIL and GBL on potato cultivation

From the lender’s operational and financial perspective, the TRAIL scheme outperformed the GBL scheme: initial take-up rates were higher, average repayment rates across six cycles were slightly higher (98% vs. 91%), and at the end of six cycles 80% of the original borrowers continued to participate, as opposed to 60% in the GBL scheme. The costs of administering the TRAIL scheme were also considerably lower because the TRAIL loans did not require monthly meetings or monitoring by MFI officials. Thus the scheme had a larger impact on credit access, generated larger revenues, and imposed lower costs on the MFI, making it unambiguously more cost-effective than the group-based lending scheme.

Implications for credit policy design

The Malegam Committee recommended that instead of banks lending directly to the rural poor, rural lending should take place through self-help groups, with Banking Correspondents and Facilitators acting as intermediaries. However there is no consensus on how the loan intermediaries should be identified, what their exact role should be, and what contractual terms they should have. Policymakers are understandably concerned about the power and influence these agents may wield, and the consequences of the abuse of such power.

Our study provides evidence on one approach to this issue. To realise high production growth and impact borrower incomes, loan durations could be extended to match crop cycles, and the focus could be shifted away from group liability to individual liability. The savings in administrative costs would allow the lender to charge substantially lower interest rates. Local intermediaries could be incentivised as in TRAIL to secure their cooperation, while ensuring checks and balances to prevent their exploiting the borrowers. Such an approach has the potential to increase financial inclusion while also making a significant dent on poverty and promoting agricultural growth.