Can easier access to credit help lift Ghanaian farmers out of poverty?

Agriculture in Ghana makes up 40% of the country’s GDP and the sector employs about 55% of the working population. However, despite their contribution of agriculture to the national economy, food crop farmers suffer from some of the highest rates of poverty.

For most, farming provides a subsistence existence and is hard toil – undertaken with traditional tools such as the hoe and the cutlass. Farms are badly irrigated and farmers have limited access to facilities that could process their produce into products that yield a higher profit.

Poor access to markets, weak infrastructure – such as roads and storage facilities –limited ability to influence government policy, as well as inadequate credit have all contributed to the agri-business sector not realising its full potential.

Considering the risks involved in agricultural production, most banks and non-bank financial institutions have shown little interest in extending credit to smallholder farmers. Furthermore, credit from formal institutions comes with demands for huge collateral and other stringent requirements that are difficult, if not impossible, for farmers to meet.

Informal sources of credit on the other hand are expensive because of the high rate of interest charged.

Selling short?

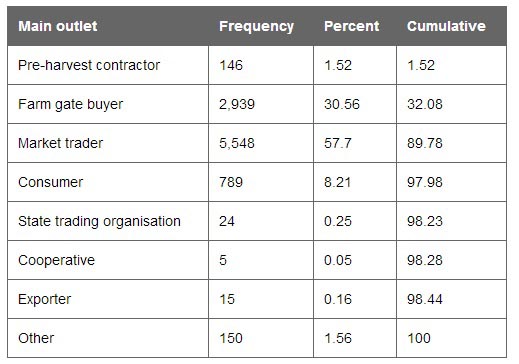

Farmers can access credit through middlemen or buyers. Our research shows that most farm produce in Ghana is sold through market traders who buy with cash or at times on credit from the farmers (Quartey et al. 2012). These traders form an important link between rural farmers and urban consumers, but they do not generally provide the best price to farmers. Instead, they often form cartels to regulate the price of produce in the urban markets while bidding down the price at the farm gate.

After market traders, producers have their wares mostly purchased by those who go directly to the farm to buy the products for their own use. Similarly, the farmers also make use of the local markets within the community to sell their produce.

Table 1 Distribution of marketing channels in 2008

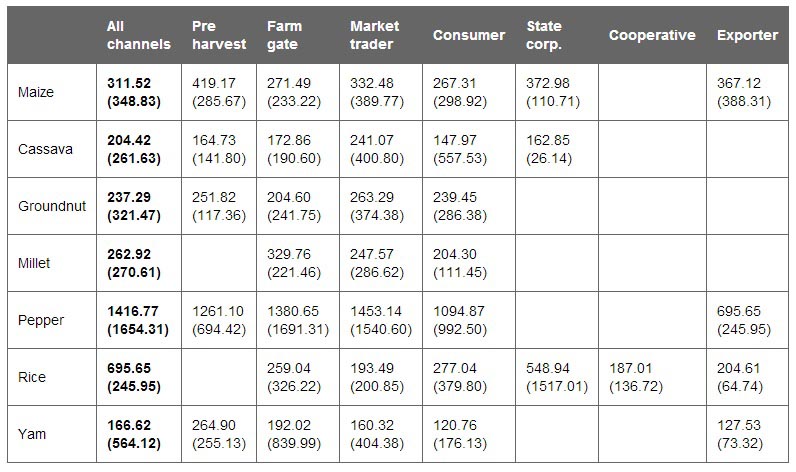

Using data from the Ghana Living Standards Survey (GLSS5+, 2008) we found that in the cassava and pepper markets, market traders offered higher average prices than the average farm-gate price. However, all other middlemen offered lower than average prices, although farm-gate buyers offered higher average prices than others

While it has been speculated that middlemen often provide credit through contracts whereby they pay a very low price for produce before it is harvested, we found that smallholder farmers seldom make use of this marketing channel. And according to the GLSS5+ 2008 data, pre-harvest contractors frequently offered farmers higher average farm-gate prices than the average price offered by all marketing channels.

Table 2 Average farmgate prices offered by the different marketing channels (2008)

Cooperatives, an alternative to middlemen and a known marketing channel for effectively guaranteeing stable prices and access to market (under certain conditions), are barely used by Ghanaian smallholder farmers. Only about 0.05% of respondents sell through this channel because most of the known farmer cooperatives, including the publicly owned cooperatives, have been dysfunctional.

Utilising technology

The rewards for farmers who are able to afford agricultural high technologies are relatively high farm-gate prices for their crops, especially for maize, groundnut and cocoyam.

For example, pest control on the farm is strongly associated with high relative farm-gate prices for especially rice, millet, cocoyam and cassava. This is probably because pest control is likely to increase the quality of the produce.

Use of improved seeds is also very important in determining the gross margin for most of the crops under study. In the case of yam, rice, millet and groundnut, the use of improved seeds bring about relatively high farm-gate prices. Just as it is in the case of pest control, the use of improved seeds may be associated with higher quality of the produce. Another possible explanation is that some farmers may have better market access (lower margins) for both output and inputs; hence they use improved seeds and pest control because they are cheaper.

On the other hand, use of improved seeds is associated with higher gross margins for cocoyam and cassava. This may be because the improved seeds are associated with increased supply of the produce in the community thereby putting a downward pressure on the farm-gate prices.

Irrigation also brings relatively higher prices for produce (except for millet) in communities, relative to communities where irrigation farming does not exist.

Farmers who are able to produce crops in lean (dry) seasons are able to get high farm-gate prices for them.

Furthermore, storage facilities in the community help farmers reduce the gross margins for maize and groundnut in particular. These facilities enable farmers to hold onto their produce when the prices being offered for them are low and sell when prices are higher.

These examples show how providing better access to credit, and thus modern farming techniques, could help improve farmers' lives. With this in mind, farmers should be educated on sources of credit and marketing channels and be encouraged to form cooperatives that would enhance their bargaining power and improve their chances of obtaining credit from formal institutions.

While the state has retreated from providing credit, marketing and other forms of support to farmers, our study suggests that it should use its regulatory powers to ensure that the agricultural sector does not suffer unduly from its privatisation and liberalisation policies.

References

Quartey, P, C Udry, S Al-hassan and H Seshie (2012) ""Agricultural financing and credit constraints: the role of middlemen in marketing and credit outcomes in Ghana"", International Growth Centre working paper.