Financing Africa: New hopes and continuous challenges

Cautious hope is in the air for finance in Africa. A deepening of financial systems can be observed in many African countries, with more financial services, especially credit, provided to more enterprises and households. New players and new products, often enabled by new technologies, have helped broaden access to financial services, especially savings and payment products.

Innovative approaches to reaching out to previously unbanked parts of the population go beyond cell phone-based M-Pesa in Kenya and basic transaction accounts, such as Mzansi accounts in South Africa (see Jack and Suri 2011). Competition and innovation dominate more and more African financial systems and for every failure there is now at least one success story. However, the benefits of deeper, broader, and cheaper finance have not been reaped yet. Finance in Africa still faces problems of scale and volatility. And the same liquidity that helps reduce volatility and fragility in the financial system is also a sign of the limited intermediation capacity.

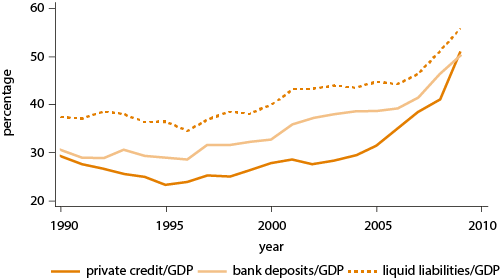

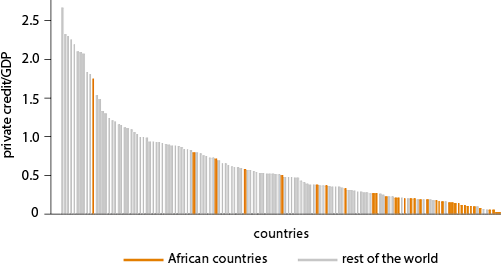

Figures 1 and 2 illustrate the challenges and opportunities for African finance. On the one hand, African financial systems are among the smallest in the world, as measured by a standard indicator, ie private credit to GDP. On the other hand, aggregate indicators show an upward trend, which started before the crisis but has picked up again afterwards.

Figure 1 Financial development in Africa over time

Source: Beck et al. (2010).

Note: Sample size = 25 countries. The number of countries indicated represents the situation following the balancing of the dataset.

Figure 2 Financial development in Africa and elsewhere

Source: Beck et al. (2010).

Note: Sample size = 140 countries. The highest African values are for Mauritius, Morocco, South Africa and Tunisia.

While the Global Financial Crisis has not affected Africa as much as other regions of the developing world – a result of its limited links with the global financial markets – several trends, some of which started before the crisis, will contribute to the future structure of finance in Africa. Take first technology. Over recent years, the transformational impact of technology on financial-system deepening and broadening has become clear. With over 13 million clients in Kenya M-Pesa is the world’s most widely used telecom-led mobile money service and other countries across the continent are seeing similar success stories (Jack and Suri 2011). The success of cell phone-based banking has also shown the possibility of increasing financial inclusion through a transaction-based rather than credit-based approach.

There also has been an increasing trend towards regional integration within the continent over the past years, though this trend started well before 2007. South African, Nigerian, Moroccan, and Kenyan banks are rapidly expanding their operations in the region. Steps towards economic and financial integration within East Africa are moving ahead and there is increased cooperation in other subregions of the continent. This comes in addition to broader trends in the global financial system, with a shift of weights away from the North (G7) towards the East (especially China and India) and South (to the G20). In the context of globalisation, the BRIC countries, especially China, India, but more recently also Brazil, have played an increasingly important role in Africa.

The new environment – globalisation, regionalisation, and technology - offer new challenges but also new opportunities for financial sectors across the region. A forthcoming joint publication by the African Development Bank, the German Federal Ministry for Economic Cooperation and Development, and the World Bank (Beck et al 2011) assesses these challenges and opportunities across three dimensions: expanding access to financial services by both households and enterprises, lengthening financial contracts, and safeguarding financial systems for their users. Across the three themes, we focus on three main messages as discussed in the following.

Competition is the most important driver of financial innovation that will help African financial systems deepen and broaden

While in the industrialised countries of North America and Western Europe, financial innovation has acquired a bad connotation after the recent crisis, being associated with CDO, CDS, and other three-letter abbreviations, financial innovation is more than that and comprises numerous new products, new processes, and new organisational forms. Recent examples in Africa include (i) mobile banking, ie access to basic payment services through mobile phones, even without having to have a bank account, (ii) the use of psychometric assessments as a viable low-cost, automated screening tool to identify high-potential entrepreneurs, (iii) agricultural insurance based on objective rainfall data, and (iv) new players in the financial systems, such as micro-deposit taking institutions, and cooperation between formal and informal financial institutions. However, financial innovation can only happen in a competitive environment.

Competition, in this context, is broadly defined and encompasses an array of policies and actions. On the broadest level, it implies a financial system that is open to new types of financial service providers, even if they are non-financial corporations. It allows the adoption of new products and technologies. The example of cell phone–based payment systems across the continent is one of the most powerful illustrations in this category. To achieve more competition in smaller financial systems, more emphasis has to be placed on regional integration. Within the banking system, competition implies low entry barriers for new entrants, but also the necessary infrastructure to foster competition, such as credit registries that allow new entrants to draw on existing information. However, this might also mean more active government involvement by, for example, forcing banks to join a shared payment platform or contributing negative and positive information to credit registries. While it is important to stress that the focus on innovation and competition should not lead to the neglect of financial stability, there has been a tendency in many African countries to err too much on the side of stability.

There is a need to focus more on financial services and less on specific institutions

While most of the analysis and policy recommendations focus traditionally on specific institutions or markets, we care primarily about the necessary financial services and, only in the second instance, about the institutions or markets that provide the services. Africa’s financial systems are heavily bank-based, in line with their level of financial and economic development. Capital markets are small and – where they exist – mostly illiquid. Contractual savings institutions, such as insurance companies and private pension funds, are underdeveloped and often poorly managed and supervised. There is a need to diversify financial systems away from a heavily bank-dominated system, but it is also important to recognise that artificially creating certain components of the financial system without the necessary demand and infrastructure will have limited economic benefits.

Banks are and will continue for a long time to be the most important component of African finance, but if non-banks are better at providing certain financial services, they should be allowed to do so. If the small economies of Africa cannot sustain organised exchanges, the emphasis should be placed instead on alternative sources of equity finance, such as private-equity funds. If the local economy is not sufficiently large to sustain certain segments of a financial system, then the importation of such services should be considered, eg, in the form of regional stock exchanges and listing. One size does not fit all; smaller and low-income countries are less able than larger and middle-income countries to sustain a large and diversified financial system and might have to rely more heavily on international integration.

There is a need for increased attention to the users of financial services

While the focus has been on supply-side constraints, partly driven by data availability, a more prominent focus of analysis and policy should be on the (potential) users of financial services. Turning unbanked enterprises and households into a bankable population and ultimately banked customers involves more than pushing financial institutions down-market. Achieving such a change requires financial literacy, that is, knowledge about products and the capability to make good financial decisions among households and enterprises (Jappelli and Padula 2011). It also means that non-financial constraints must be addressed, such as the business environment and access to markets, most prominently in agriculture. It includes a stronger emphasis on equity financing for often overleveraged enterprises. It also includes a consumer-protection framework, which includes (i) consumer disclosure that is clear, simple, easy to understand, and comparable; (ii) prohibitions on business practices that are unfair, abusive, or deceptive; and (iii) efficient and easy-to-use recourse mechanisms.

All financial-sector policy is local

Africa’s problem has not been in the choice of the ‘solutions’ but rather, the direction and quality of their application to local circumstances, and the failure to build or scale up home-grown solutions. Unless there are changes in the politics of financial reforms in Africa, even the recent opportunities of globalisation, technology, and regional integration will suffer the same fate as others that once promised to resolve Africa’s financial constraints. While modernisation represents the bedrock of any credible vision for national financial sectors, whether in Africa or elsewhere, the problem has been the application of the modernist agenda on the primary premise that modernisation is equivalent to “best practice” of the advanced market economies. Unless policymakers and development partners that work with them deliberately redefine progress in financial-sector development to suit local African conditions, the modernist agenda will continue to overreach in Africa. In the end, all financial-sector policy is local.

This column first appeared on www.VoxEU.org. Reproduced with permission.

Further reading

Beck, T, A Demirguc-Kunt and R Levine (2010), “Financial Institutions and Markets Across Countries and Over Time: The Updated Financial Development and Structure Database.” World Bank Economic Review 24, 77-92.

Beck, T, S Munzele Maimbo, I Faye and T Trik (2011), Financing Africa: Through the Crisis and Beyond, Washington, DC: World Bank.

Jack, W and T Suri (2011), “Mobile Money.” VoxEU.org, 16 March.

Jappelli, T and M Padula (2011), “Investment in Financial Literacy and Saving Decisions” VoxEU.org, 8 February.

- See more at: http://www.ideasforafrica.net/articles/financing-africa-new-hopes-and-continuous-challenges#sthash.P7pQxE2o.dpuf"