Impact of the Russia-Ukraine war on Ethiopia

The conflict in Ukraine and the subsequent sanctions against Russia triggered price increases of key commodities with far reaching impacts on welfare, production, and economic growth for developing countries, including Ethiopia.

Economic sanctions were imposed on Russia by the US and EU to deter Russia from further escalating the war with Ukraine. The ongoing conflict has caused severe supply disruptions, resulting in sharp price increases for commodities of which Russia and Ukraine are large global suppliers as well as their close substitutes. Prices of essential commodities like grain, petroleum, and fertiliser have consequently surged significantly. This, in turn, can severely affect welfare in terms of higher food and energy prices and can also undermine productive capacity as essential inputs for agricultural and non-agricultural production become more expensive. To estimate the extent of the impact, we simulate the impact of price increases for key commodities on production, employment, and household welfare in Ethiopia.

Rising prices of key commodities and imports

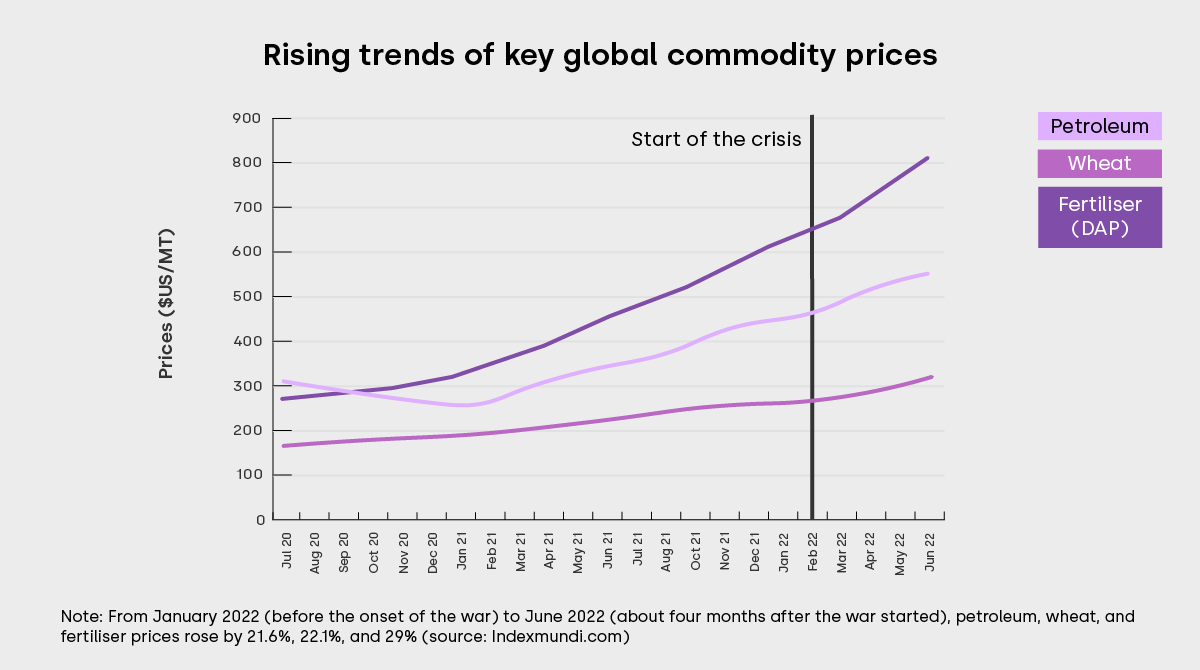

Ethiopia, along with the rest of the world, experienced a sharp rise in prices of key commodities with the onset of the war in Ukraine (figure 1). The 12-month moving average price of crude brent petroleum in June 2022 increased by 64% from June 2021 while the price of wheat increased by 48%, with edible oil prices increasing by roughly 49% in the same period. Similarly, given that Russia is the biggest exporter of nitrogen-based fertiliser, the second and third most important global supplier of potassium and phosphate respectively, the Russia-Ukraine war has impeded supply and led to global increases in their prices.

Figure 1

Note: From January 2022 (before the onset of the war) to June 2022 (about four months after the war started), petroleum, wheat, and fertiliser prices rose by 21.6%, 22.1%, and 29% (source: Indexmundi.com).

Such significant global commodity price shocks especially affect developing countries that are net food and oil importers. Ethiopia, for instance (as of 2021), imports close to US$ 3 billion worth of petroleum products, accounting for a fifth of total merchandise imports and equivalent in monetary value to the country’s total merchandise exports. The country also imports close to US$ 2 billion worth of fertilisers, accounting for almost the entire domestic supply of this commodity. Wheat imports total around US$ 400 million per year (depending on exchange rate and purchase price) and account for about a quarter of total domestic consumption of this product. Additional imports of significance are metal and edible oils. In total, the monetary import value of these commodities accounts for a third of total merchandise imports and is equivalent to twice the value of Ethiopia’s merchandise exports. This shows how significant these commodities are to the balance of payments and the strain price increases would cause on agricultural production and food consumption. Persistent global price increases may lead to either further balance of payments deficits or a decline in essential commodity imports for the next fiscal year. The timing of this shock is further exacerbating, as even though Ethiopia was on the path to recovery from COVID-19, it was simultaneously reeling under the effect of an internal conflict in its northern and western parts since November 2020.

Simulating the impact of the war on key economic sectors and commodities

On top of the direct impact on the import bill, the crisis also affects production and consumption. We use a Computable General Equilibrium (CGE) model to simulate the effects on production and consumption employing a recursive Dynamic Stochastic Computable General Equilibrium (DSCGE) model developed by the International Food Policy Research Institute (IFPRI).

For our analysis, we simulate the direct and indirect effects of the Russia-Ukraine war on the Ethiopian economy as a shock from increased international prices for five key import items/groups (wheat, edible oil, metal and metal products, fertiliser, and petroleum) relative to a pre-war shock. To do so, we set up two simulation scenarios. The first is a business-as-usual (BAU) reference scenario using the growth rate of the last two years before the Ukrainian crisis. This scenario implicitly contains the impact of COVID-19 and other natural and human-made crises during the period. The second scenario is the Russia-Ukraine war induced global shock scenario that reflects current global prices of the five import item groups considered in the analysis. The overall findings, hence, compare the Russia-Ukraine war shock scenario with the BAU scenario.

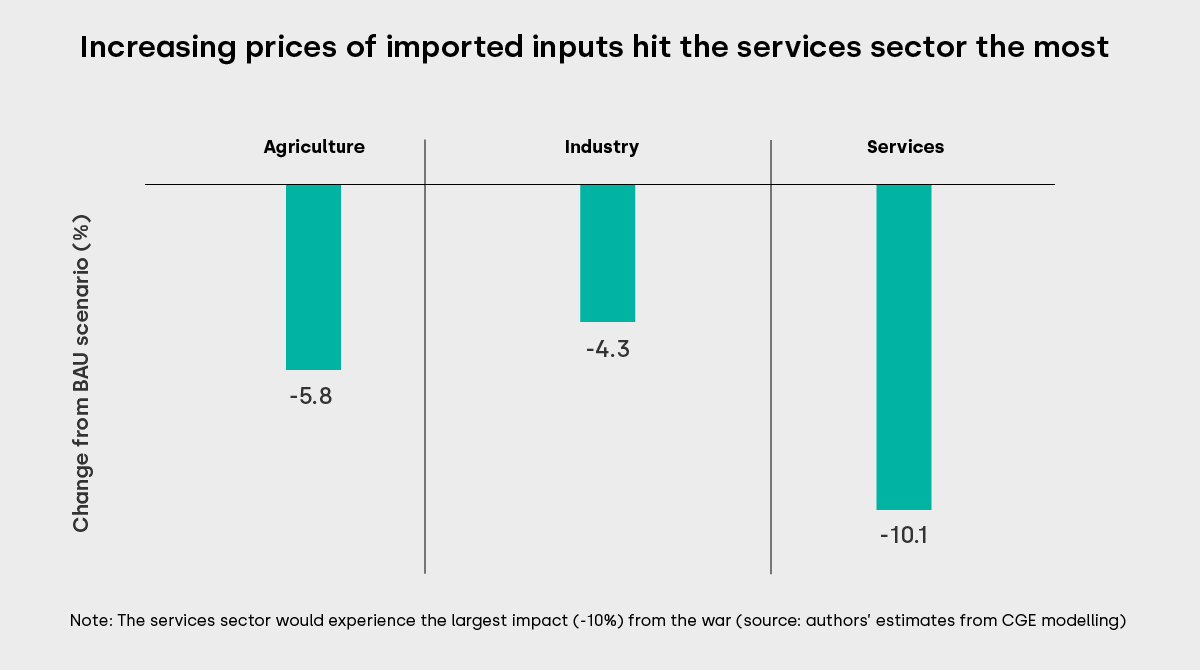

Services sector would be most affected by higher input prices

From the simulation, petroleum prices would increase by 86% compared to their value in 2021-22. Similarly, prices of wheat, edible oil, DAP fertiliser, and metal products would increase by 100%, 11%, 108%, and 82% respectively. Figure 2 below portrays the potential impacts on the major economic sectors – agriculture, industry, and services. Results show that the services sector would be the hardest hit amid the ongoing Russia-Ukraine crisis followed by the agriculture sector. The services sector is the prime user of fuel through transport services and this has considerable implications for other sectors like wholesale and retail trading. The services sector is also negatively affected through the real-estate sub-sector that could be impacted by the higher prices of metal and metal products. The effect on agriculture could be through a direct fertiliser price increment or an indirect price effect through higher transportation costs (fuel). The industry sector would be moderately affected probably through a direct impact on construction material like metal and metal products.

Figure 2

Note: The services sector would experience the largest impact (-10%) from the war (source: authors’ estimates from CGE modelling)

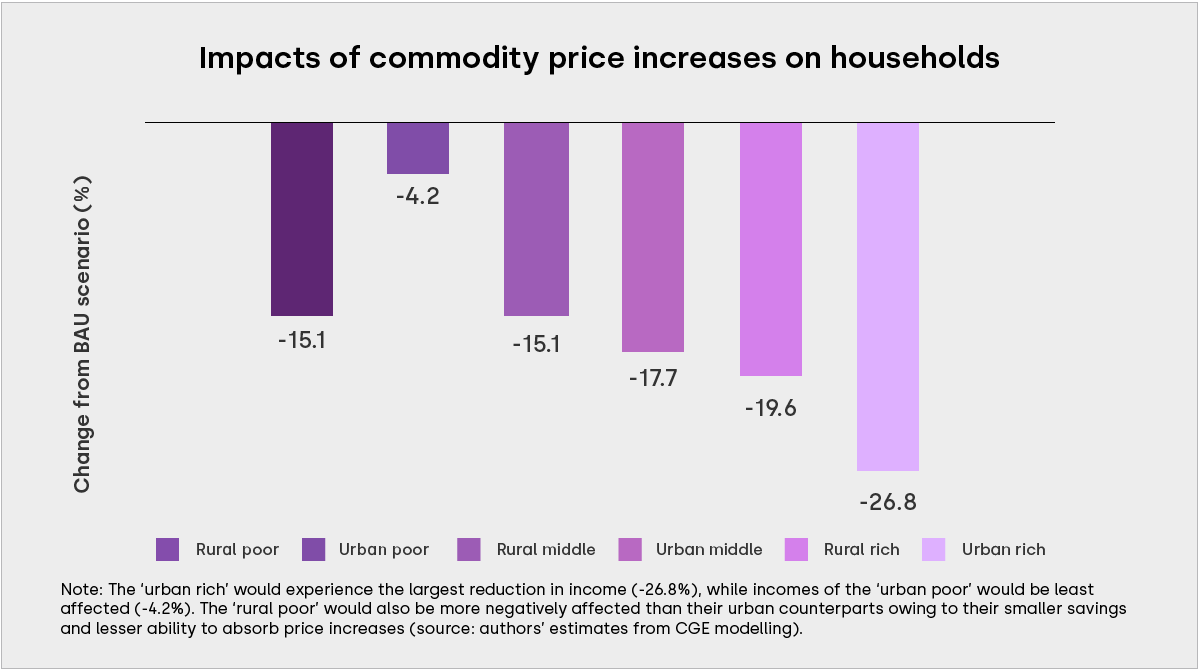

Rural poor households would be the worst hit

For the income distribution impact of the price shocks, the rich and middle-income groups in both urban and rural areas would generally be more negatively affected by the crisis. The rural rich and middle-income households are potentially partially compensated by the increased prices of the agricultural goods they produce but not sufficiently. This could be due to a strong cross-price elasticity between wheat and the other major cereals (for example, maize, teff, sorghum) which show similar price changes. While the urban rich households see the largest decrease in incomes, the rural poor suffer more than their urban counterparts as they have lower levels of savings and less capacity to absorb price increases, since their basic necessities take up a larger share of their household budget.

Figure 3

Note: The ‘urban rich’ would experience the largest reduction in income (-26.8%), while incomes of the ‘urban poor’ would be least affected (-4.2%). The ‘rural poor’ would also be more negatively affected than their urban counterparts owing to their smaller savings and lesser ability to absorb price increases (source: authors’ estimates from CGE modelling).

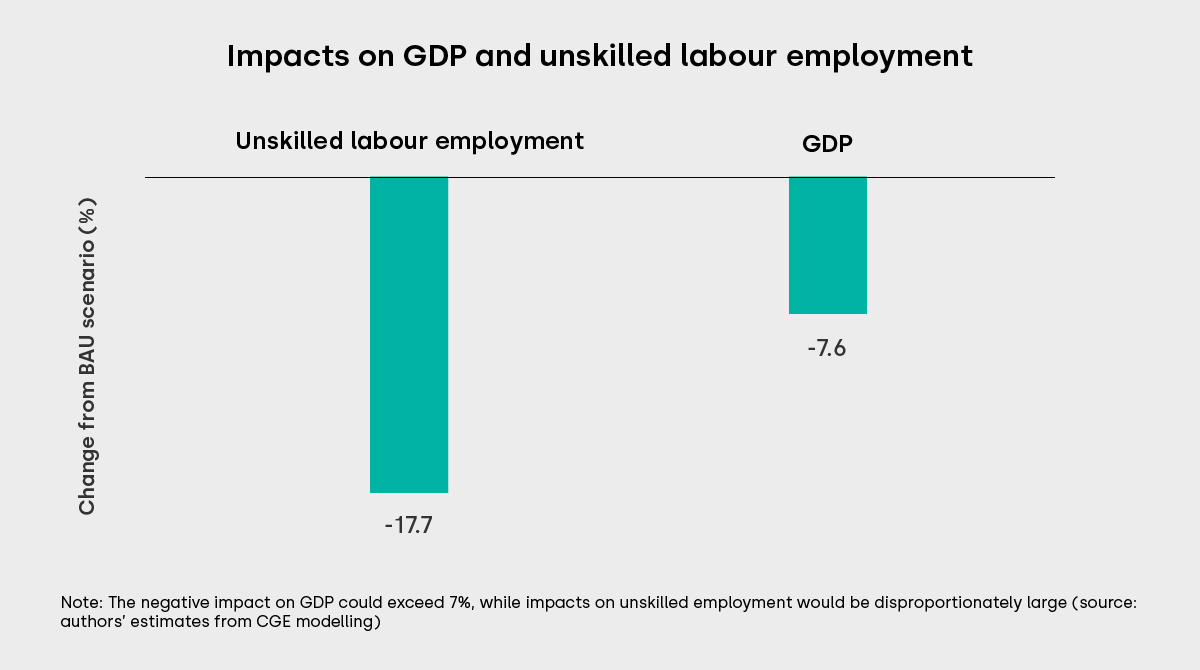

Falling GDP and employment rate for unskilled labour

Figure 4 below shows the effect of the shock on the overall economy proxied by GDP which would fall by as much as 7.6% as compared to the BAU scenario. Given the contribution of the services and agriculture sector in the overall economy in Ethiopia, it is not surprising that the effect on the overall economy is driven by the proportionally large negative impact on the services and agriculture sectors. For example, in 2021, the two sectors together accounted for more than 72% of the GDP: services (39.6%) and agriculture (32.5%). The figure also looks at employment changes for unskilled labour that, according to the latest Ethiopian Social Accounting Matrix (SAM), account for about 78% of the labour force. In line with the considerably larger proportion of the unskilled labour in the overall labour force, it is likely that the bulk of adjustment falls on the unskilled labour in the severely affected sectors-i.e., services and agriculture. Accordingly, as portrayed in the figure, the magnitude of employment loss would be significant at about 18%, therefore necessitating the consideration of mitigation measures.

Figure 4

Note: The negative impact on GDP could exceed 7%, while impacts on unskilled employment would be disproportionately large (source: authors’ estimates from CGE modelling)

Mitigating the impacts of global commodity shocks

The global shocks resulting from the Russia-Ukraine war will have severe consequences. Keeping in mind the magnitude of the shock and the fact that Ethiopia has no market power to affect prices, Ethiopia cannot be insulated from global commodity shocks. However, there are potential measures that can be taken to reduce the negative impacts of the shock and identify opportunities to use the crisis to expand other exports and stimulate domestic production through import substitution.

Targeted lifting of fuel subsidies

In light of the rising import costs, efficient use of imported commodities like fuel will have to be encouraged. The fuel subsidy for all fuel users was fiscally challenging, prompting the government to lift the subsidy starting July 2022. The removal of the subsidy is expected to raise all transportation costs with ripple effects throughout the economy. The government has however, already started the commendable process of differentiated subsidies targeting only vehicles that provide public transport services. For energy more broadly, Ethiopia’s heavy reliance on hydropower would mute the impact of the oil price shock. In fact, the shock may further whet the appetite of other countries in the region to tap into Ethiopia’s hydropower potential.

Potential for import substitution and increased local production

Fertiliser: A similar measure would be to replace imported nitrogen-based fertilisers with local substitutes like animal waste and compost. The government has already started encouraging farmers and households to prepare compost from waste of vegetables and fruits. It is also important to secure supply commitments given the cut-offs from Ukraine and Russia. Again, the government was successful in renegotiating a major fertiliser contract, albeit with likely reductions in imported fertiliser.

Edible oils: While the major cooking oil consumed by Ethiopians, particularly the poor is palm oil, there is scope for substitution to domestic production and further work on this sub-sector is forthcoming. More generally, the implicit pressure on imports of other commodities including processed food could present an opportunity to reenergise domestic agro-processing capacity servicing the middle- and higher-income urban consumers. This would help reinforce reforms anticipated under the emerging revised industrial policy.

Metals: The major use of imports is construction. The shock in prices will likely negatively affect development projects by increasing their overall cost. This would require phasing of development projects to focus on the completion of the highest priority ones.

Opportunities for commodity export growth

Most of the attention has rightly focused on key imported commodities. However, at the same time the Ukraine-Russia crises may also open up opportunities for exports of commodities that have been cut off from Russia and Ukraine’s supplies and where Ethiopia can position itself as an alternative supplier. One such example may be gold and other minerals for which Russia and the Ukraine are also important global suppliers. For instance, amid recent reforms like the raising of the gold price premium from 29% to 35% in addition to a reduction (from 500 grams to 50 grams) in the requisite quantity to access this premium, gold exports have increased substantially. Gold is now Ethiopia’s most important export commodity. In addition, there has recently been increased momentum to exploit Ethiopia’s iron ore.

Nonetheless, despite best efforts at macroeconomic management, the shocks will take their toll in the short- to medium-term and feed into domestic inflation more widely. The poor will be particularly vulnerable, even if the percentage impact on their incomes is lower than that of middle- and high-income groups. It will therefore, be critical to assess targeted subsidies (such as certain types of cooking oil and transport) as well as leverage the existing rural and urban safety net programmes to help them weather the crisis.